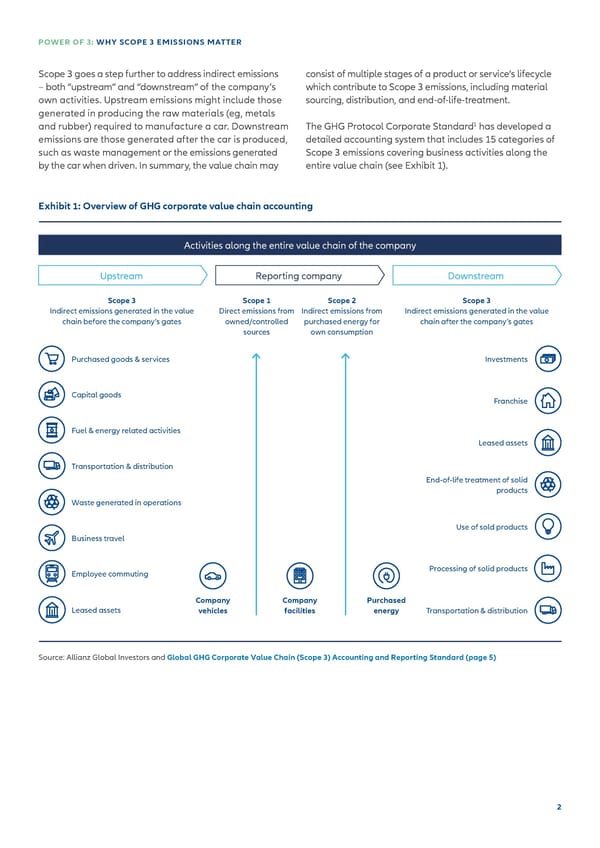

POWER OF 3: WHY SCOPE 3 EMISSIONS MATTER Scope 3 goes a step further to address indirect emissions consist of multiple stages of a product or service’s lifecycle – both “upstream” and “downstream” of the company’s which contribute to Scope 3 emissions, including material own activities. Upstream emissions might include those sourcing, distribution, and end-of-life-treatment. generated in producing the raw materials (eg, metals 1 and rubber) required to manufacture a car. Downstream The GHG Protocol Corporate Standard has developed a emissions are those generated after the car is produced, detailed accounting system that includes 15 categories of such as waste management or the emissions generated Scope 3 emissions covering business activities along the by the car when driven. In summary, the value chain may entire value chain (see Exhibit 1). Exhibit 1: Overview of GHG corporate value chain accounting Activities along the entire value chain of the company Upstream Reporting company Downstream Scope 3 Scope 1 Scope 2 Scope 3 Indirect emissions generated in the value Direct emissions from Indirect emissions from Indirect emissions generated in the value chain before the company’s gates owned/controlled purchased energy for chain after the company’s gates sources own consumption Purchased goods & services Investments Capital goods Franchise Fuel & energy related activities Leased assets Transportation & distribution End-of-life treatment of solid products Waste generated in operations Use of sold products Business travel Employee commuting Processing of solid products Company Company Purchased Leased assets vehicles facilities energy Transportation & distribution Source: Allianz Global Investors and Global GHG Corporate Value Chain (Scope 3) Accounting and Reporting Standard (page 5) 2

Scope 3 Emissions Page 1 Page 3

Scope 3 Emissions Page 1 Page 3