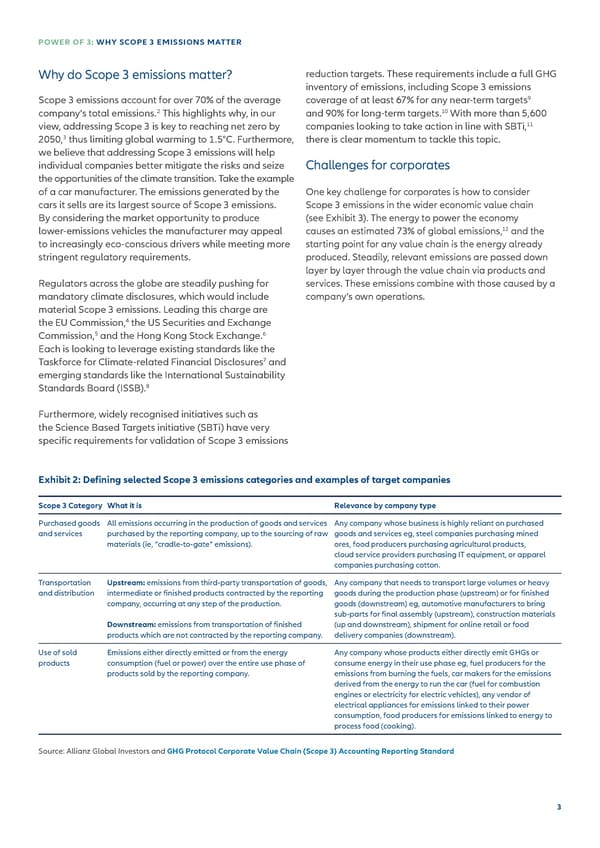

POWER OF 3: WHY SCOPE 3 EMISSIONS MATTER Why do Scope 3 emissions matter? reduction targets. These requirements include a full GHG inventory of emissions, including Scope 3 emissions Scope 3 emissions account for over 70% of the average coverage of at least 67% for any near-term targets9 2 10 company’s total emissions. This highlights why, in our and 90% for long-term targets. With more than 5,600 11 view, addressing Scope 3 is key to reaching net zero by companies looking to take action in line with SBTi, 2050,3 thus limiting global warming to 1.5°C. Furthermore, there is clear momentum to tackle this topic. we believe that addressing Scope 3 emissions will help individual companies better mitigate the risks and seize Challenges for corporates the opportunities of the climate transition. Take the example of a car manufacturer. The emissions generated by the One key challenge for corporates is how to consider cars it sells are its largest source of Scope 3 emissions. Scope 3 emissions in the wider economic value chain By considering the market opportunity to produce (see Exhibit 3). The energy to power the economy 12 lower-emissions vehicles the manufacturer may appeal causes an estimated 73% of global emissions, and the to increasingly eco-conscious drivers while meeting more starting point for any value chain is the energy already stringent regulatory requirements. produced. Steadily, relevant emissions are passed down layer by layer through the value chain via products and Regulators across the globe are steadily pushing for services. These emissions combine with those caused by a mandatory climate disclosures, which would include company’s own operations. material Scope 3 emissions. Leading this charge are 4 the EU Commission, the US Securities and Exchange Commission,5 and the Hong Kong Stock Exchange.6 Each is looking to leverage existing standards like the 7 Taskforce for Climate-related Financial Disclosures and emerging standards like the International Sustainability Standards Board (ISSB).8 Furthermore, widely recognised initiatives such as the Science Based Targets initiative (SBTi) have very speci昀椀c requirements for validation of Scope 3 emissions Exhibit 2: De昀椀ning selected Scope 3 emissions categories and examples of target companies Scope 3 Category What it is Relevance by company type Purchased goods All emissions occurring in the production of goods and services Any company whose business is highly reliant on purchased and services purchased by the reporting company, up to the sourcing of raw goods and services eg, steel companies purchasing mined materials (ie, “cradle-to-gate” emissions). ores, food producers purchasing agricultural products, cloud service providers purchasing IT equipment, or apparel companies purchasing cotton. Transportation Upstream: emissions from third-party transportation of goods, Any company that needs to transport large volumes or heavy and distribution intermediate or 昀椀nished products contracted by the reporting goods during the production phase (upstream) or for 昀椀nished company, occurring at any step of the production. goods (downstream) eg, automotive manufacturers to bring sub-parts for 昀椀nal assembly (upstream), construction materials Downstream: emissions from transportation of 昀椀nished (up and downstream), shipment for online retail or food products which are not contracted by the reporting company. delivery companies (downstream). Use of sold Emissions either directly emitted or from the energy Any company whose products either directly emit GHGs or products consumption (fuel or power) over the entire use phase of consume energy in their use phase eg, fuel producers for the products sold by the reporting company. emissions from burning the fuels, car makers for the emissions derived from the energy to run the car (fuel for combustion engines or electricity for electric vehicles), any vendor of electrical appliances for emissions linked to their power consumption, food producers for emissions linked to energy to process food (cooking). Source: Allianz Global Investors and GHG Protocol Corporate Value Chain (Scope 3) Accounting Reporting Standard 3

Scope 3 Emissions Page 2 Page 4

Scope 3 Emissions Page 2 Page 4